Assets in Asia – currencies, stocks, and bonds – keep struggling under the collective weight of global drivers: U.S. interest rates, China growth, the Japanese yen, and the manufacturing export cycle. When these factors pushed in the same bearish direction at various points during the past year and early 2024, the sum of fears led to bad outcomes across broad swathes of asset classes and countries. Lower yielding Asian currencies could not withstand the rise in U.S. interest rates and equity markets that were dependent on Chinese demand underperformed; currencies that were traditionally correlated to the depreciating yen were bogged down, while Asia’s newly industrial economies struggled through the global manufacturing downturn.

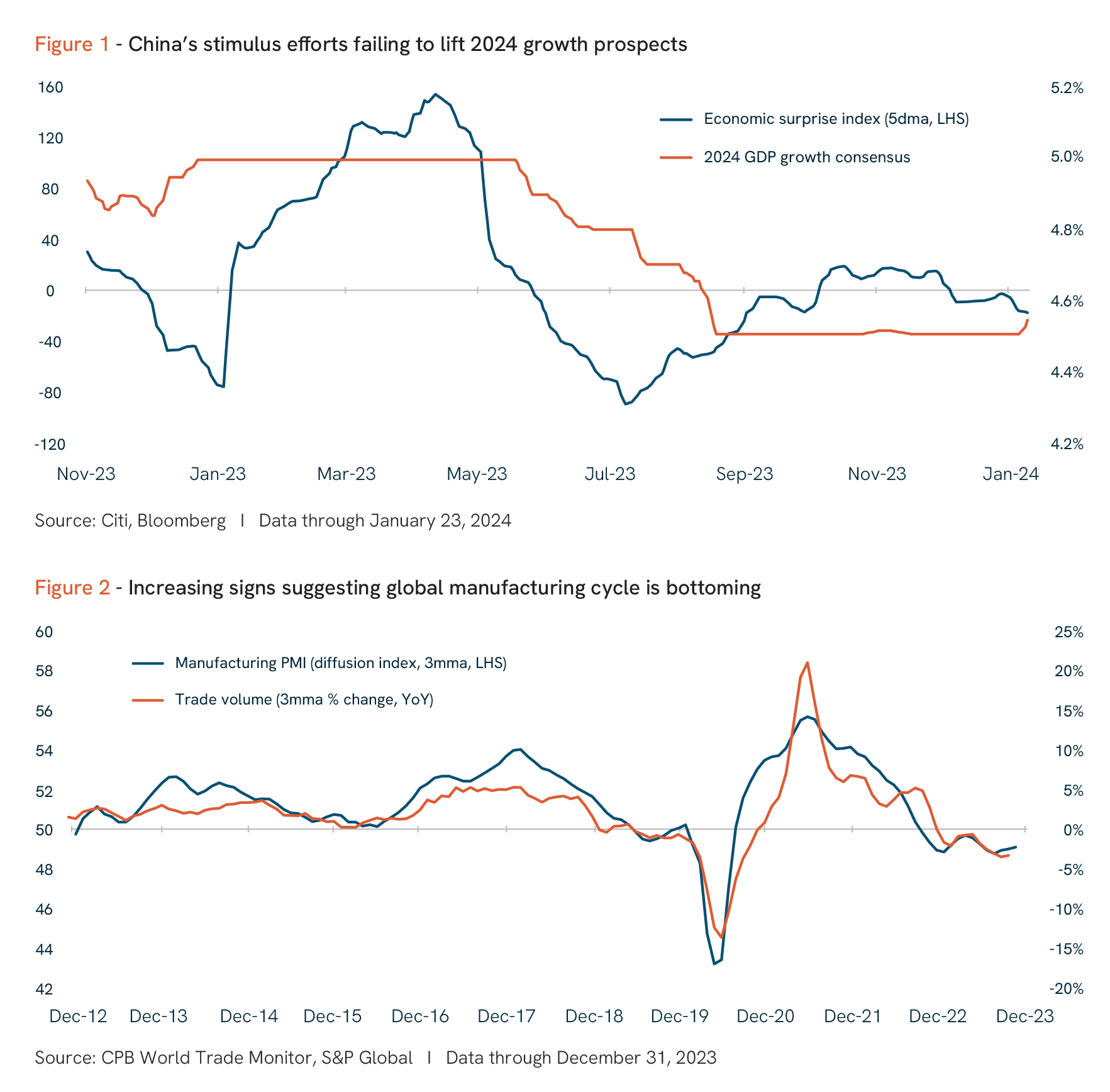

What are the odds of these fears receding over the course of 2024, opening the door for Asian assets to perform? A bullish, balanced growth scenario for Asia involves several pieces, some of which are gradually falling in place. The first is inflation in the U.S. showing further progress towards the 2% target without requiring a deep recession. China underwrites 2024 growth with the right mix of fiscal, monetary, and housing policies; meanwhile, Japan at some point ends its negative interest rate policy (NIRP), narrowing monetary policy divergence that has resulted in the loss of the Japanese yen as a key currency anchor for Asia (see Figure 1). The early-stage export recovery, now visible in Asia’s tech space, is moving towards firmer ground (see Figure 2). Lastly, geopolitical tensions do not threaten energy prices and sentiment. A combination of these developments would allow Asian central banks to better calibrate monetary policy according to their internal objectives instead of being beholden to U.S. rates and the dollar, and for Asia and broader emerging market (“EM”) assets to outperform.

• Four global drivers – U.S. interest rates, China growth, the Japanese yen, and the manufacturing export cycle – keep weighing on Asian assets.

• The odds that some of these headwinds will recede during 2024 seem to be rising, with positive implications for Asian markets and emerging market performance more broadly.

The debate about the U.S. Federal Reserve (the “Fed”) is shifting towards the timing of rate cuts. There is now greater visibility that inflation is making progress on the last mile towards the 2% target, although sticky services inflation remains a concern. Markets have been choppy in the first trading weeks of 2024, as interest rate market pricing of overly aggressive Fed cuts, expecting either quick inflation relief or growth weakness, has been vulnerable to incoming data that showed otherwise. Clearer signs of disinflation, would simultaneously assuage growth and interest rate fears, forming a stronger basis for a risk rally to take place.

A central uncertainty for 2024 is whether a U.S. recession will ultimately be required to bring inflation to target. There are reasons to believe that, barring a major financial accident, a U.S. recession – if any – will be mild. Drags from monetary policy have been offset in part by the recent loosening of financial conditions, while private consumption remains supported by income growth amid a resilient labor market. A remarkable feature in the present cycle is that the U.S. sacrifice ratio (the rise in the unemployment rate associated with a fall in inflation) has been so low. Some unusual dynamics in the U.S. labor market have been responsible for the avoidance of recession thus far. Firms have reduced job openings on offer, cooling off wage pressures without entailing a large sacrifice in the form of actual job losses. Should this unprecedented combination of falling job openings, low unemployment, and moderating wage growth persist in 2024, we believe there is a better than even chance that inflation can continue to cool off without precipitating a recession in the U.S.

A scenario of continued U.S. growth resilience with persistent high rates, which today looks less likely, will be challenging for the world. Asia ultimately requires balanced global growth, specifically for the EU to show firmer signs of recovery given its importance as a source of final demand. U.S. exceptionalism that results in higher global interest rates and a stronger dollar has done more harm than good in 2023. Asia and broader EM cannot perform well in a world where only one cylinder of the global growth engine is firing.

Economic forecasting in 2024 will by no means be easier than in 2023. Widely held predictions in late-2022 for a U.S. recession in 2023 and a strong China post-reopening rebound, for example, did not materialize. The distortionary effects from Covid-19, both in the goods and labor markets, continue to linger and disrupt historical economic relationships. The pandemic unleashed an unprecedented combination of major demand and supply shocks that impacted the goods and services sectors differently. This combination caused discontinuous shifts that amplified price pressures long after supply in the durable goods sector normalized, particularly in countries where the fiscal impulse pushed in the same direction as robust private spending. Thus, growth was more resilient and inflation more persistent in 2023 than initially believed.

One risk to markets is that the legacy of these distortions continues to lurk in the background and put upward pressure on term premia and long-term rates. Should fiscal deficits prove to be persistent as U.S. social spending needs increase, the equilibrium real interest rate (or r*) will continue to increase. The demand-supply balance of U.S. treasuries could deteriorate, given the need for greater issuance, and the shift of bond demand towards more price sensitive buyers as central banks reduce bond purchases as they shift from quantitative easing to quantitative tightening. Future U.S. Treasury auctions need to be taken up with sufficient demand for term-premia to stay orderly.

Meanwhile, China continues to deliver bite-sized stimulus in the monetary, fiscal, and property spaces. The Central Economic Work Conference late last year tilted towards a pro-growth stance for 2024 and recommended the use of stronger counter-cyclical policies to revive the economy. This message came after a higher fiscal deficit target, as well as plans to restructure local government debt and raise targeted housing support were unveiled. We believe the People’s Bank of China’s recent announcement of a 50bp cut in the reserve requirement ratio and 25bps of cuts for relending and rediscount rates has taken monetary policy in the right direction but needs to be accompanied by stronger pro-growth policies to boost credit demand. Incremental steps in policy easing will do little to address persistent deflation and sluggish demand; a more convincing stimulus rollout (with greater specifics) is required to assuage China growth fears in our view.

Even as China’s economy fails to gain momentum, there are growing signs that tech manufacturing downcycle is subsiding. The latest evidence came from Taiwan Semiconductor Manufacturing Company’s upbeat mid-January guidance for rising revenues and capex in 2024, citing strong AI-related demand. The news from the chipmaker came after December exports from Korea surprised to the upside on a 22% annual jump in semiconductor shipments; Taiwan exports (up 12% from a year ago), also topped expectations in December. Should these green shoots in the tech space become more evident, Asia’s electronics exporters - Korea, Taiwan, Singapore, Malaysia, and Thailand – will be beneficiaries of equity inflows and begin to form an interesting axis of differentiation in 2024.

Vincent Low

Vincent has over 30 years of experience in covering global macroeconomics and markets. He is responsible for formulating investment ideas with PMs, strategists, and equity analysts and developing macro investment themes and processes for TRG’s public markets business. Prior to rejoining TRG, where he was previously CEO of its Singapore office and an Executive Committee member, Vincent held the role of Advisor to the Economics Policy Group at the Monetary Authority of Singapore. He also held roles as the Head of Currency and Fixed Income Strategy at Merrill Lynch, and Senior Economist for Southeast Asia at J.P. Morgan and Standard Chartered Bank. Vincent started his career at the Monetary Authority of Singapore in 1987 and received a Bachelor of Social Sciences in Economics from the National University of Singapore.

Luis Arcentales

Luis has over 20 years of experience in covering global macroeconomics and markets. He is responsible for formulating market strategy at TRG. Prior to joining TRG, he had a short stint as an independent macro researcher following a nearly two-decade career at Morgan Stanley in New York. In his role as Senior Economist, his primary focus was developing the macroeconomic and political outlooks for countries in Latin America, in addition to publishing on topics ranging from the business cycle to trade dynamics for the region. Luis started his career as an equity strategist at McGlinn Capital, a value-oriented asset manager in Pennsylvania. He holds an MS in Economics and a BA in Industrial Engineering from Lehigh University; he sits on the board of Lehigh’s Martindale Center for the Study of Private Enterprise and is a CFA charter holder.

DISCLAIMER

The information provided herein is for educational and informational purposes only, and neither The Rohatyn Group nor any of its affiliates (together, “TRG”) is offering any product or service hereby. The information provided herein is not a recommendation, offer, or solicitation of an offer to buy or sell any security, commodity, or derivative, nor is it a recommendation to adopt any investment strategy or otherwise to be construed as investment advice. Any projections, market outlooks, investment outlooks or estimates included herein are forward-looking statements, are based upon certain assumptions, and should not be construed as an indication that certain circumstances or events will actually occur. Other circumstances or events that were not anticipated or considered may occur and may lead to materially different outcomes. The information provided herein should not be used as the basis for making any investment decision.

Unless otherwise noted, the views expressed in the content herein reflect those of the authors as of the date published and are not necessarily the views of TRG. In fact the views of TRG (and other asset managers) may diverge significantly from certain of the views expressed in the content herein. The views expressed in the content herein are subject to change without notice, and TRG disclaims any responsibility to furnish updated information in the event of any such change in views. Certain information contained herein has been obtained from third-party sources. While TRG deems such sources to be reliable, TRG cannot and does not warrant the information to be accurate, complete or timely, and TRG disclaims any responsibility for any loss or damage arising from reliance upon such third-party information or any other content provided herein. Exposure to emerging markets generally entails greater risks and higher volatility than exposure to well-developed markets, including significant legal, economic and political risks. The prices of emerging market exchange rates, securities and other assets are often highly volatile and movements in such prices are influenced by, among other things, interest rates, changing market supply and demand, external market forces (particularly in relation to major trading partners), trade, fiscal and monetary programs, policies of governments and international political and economic events and policies. All investments entail risks, including possible loss of principal. Past performance is not necessarily indicative of future performance.

The information provided herein is neither tax nor legal advice. You must consult with your own tax and legal advisors regarding your particular circumstances.