The sentiment towards emerging markets (“EM”) at the IMF/World Bank meetings was cautiously optimistic as synchronized economic strength allowed economies to better deal with the potential headwind from higher for longer U.S. rates. The interaction between fiscal and monetary policies, plus the rebalancing processes advancing in many emerging economies, also ranked high on investors’ radar screens. The Rohatyn Group’s (“TRG”) head of public markets, Bernard Steinberg, and strategist, Luis Arcentales, discuss the main takeaways from these meetings and their implications for markets.

The sentiment towards emerging markets (“EM”) at the IMF/World Bank meetings was cautiously optimistic as synchronized economic strength allowed economies to better deal with the potential headwind from higher for longer U.S. rates. The interaction between fiscal and monetary policies, plus the rebalancing processes advancing in many emerging economies, also ranked high on investors’ radar screens. The Rohatyn Group’s (“TRG”) head of public markets, Bernard Steinberg, and strategist, Luis Arcentales, discuss the main takeaways from these meetings and their implications for markets.

Luis: Hi Bernard. I’ve been following some of the panels from the IMF meetings in D.C. last week, which dealt with some timely issues such as the need to rein in fiscal spending and to build buffers, as well as challenges from rising debt and difficulties with the last mile of disinflation. Since you were there, I want to hear what you learned from the conversations you had with EM policymakers and other investors.

Bernard: It was an intense week of meetings at a very interesting juncture for global markets. Everyone was trying to form a view on the path forward for interest rates and, more specifically, if the Federal Reserve (the “Fed”) staying on hold this year would derail risk sentiment.

Luis: That makes sense. The global scenario has quickly morphed from a high conviction that Fed cuts were on the way amid steady disinflation, to concerns about sticky inflation and higher for longer rates. The repricing brought with it higher yields, wobbly stocks, and a jump in commodity prices.

What were investors saying about the prospects for EM?

Bernard: In general, I found sentiment towards EM to be on the constructive side. The backdrop of inflation and rates, as you have pointed out, has become more uncertain. But I continue to hear that more synchronized economic strength helps EM better deal with higher U.S. rates and a stronger dollar. The pickup in Asian tech exports and manufacturing also came up a few times as a sign that the growth improvement has legs.

The key to all this, I think, is that markets so far are just delaying the cuts by the Fed, so the narrative of some form of soft landing is still at play. It would be a different story if bad inflation data were to force the Fed to turn decidedly hawkish – we are nowhere near there. This is an environment, I believe, where equities keep outperforming bonds.

From a longer-term viewpoint, I heard officials talk about the resilience of emerging economies in the current cycle. I know “resilience” is a word that gets thrown around a lot, but they rightly pointed out that despite many large shocks like Covid-19, inflation, and tighter financial conditions, there haven’t been any major EM crises. That’s a testament to fundamental improvements, including stronger policy frameworks, more credible central banks and, in many cases, bigger buffers, too.

Luis: Interesting. I recall thinking that if you gave me a scenario that involved a pandemic, serious supply-chain dislocations, inflation, and monetary policy shocks, a crisis seemed like a high probability scenario. Your comments reminded me of recent IMF work suggesting economic “scarring” from Covid-19 in major EM countries, meaning a durable loss in output, wasn’t as bad as feared.

So, Bernard, you are telling me that sentiment towards EM seemed cautiously optimistic, but EM covers a large group of countries. I am interested in some of the countries trying to implement long-overdue macro stabilization plans, such as Egypt, Argentina, and Turkey.

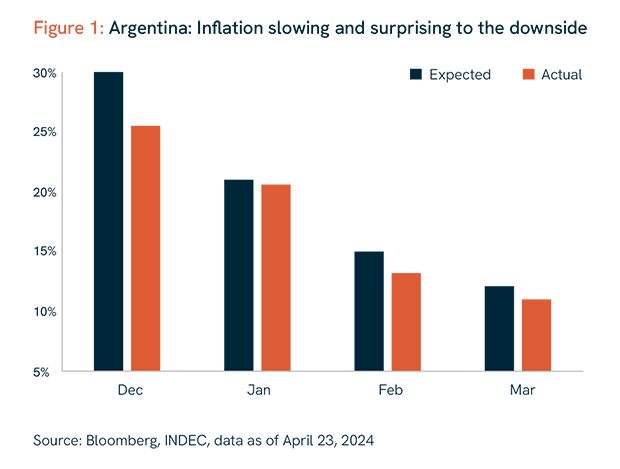

Bernard: Here is an anecdote for you: a year ago I was one of a handful of attendees to one of the Argentina sessions, and this year, it was standing room only. Investors are clearly upbeat about the fiscal adjustment and reserve accumulation while acknowledging the challenges, which means Argentina is still a trade and not yet an investment (see Figure 1). Financial repression remains in place, for example capital and FX controls, as well as negative real rates, which means there is no new money from the IMF.

The critical thing to watch is if the Milei administration can negotiate with the opposition and pass reforms, which are both necessary to make the fiscal adjustment sustainable. Without reforms, I suspect, it is hard to see a path towards a dismantling of capital controls and a sustainable recovery. In other words, you need growth to be able to pay back the debt.

Luis: How about Turkey? The recent local election dealt a blow to the incumbent and sent a clear message, I think, of voter dissatisfaction with the economy and high inflation. Any change in tone from policymakers?

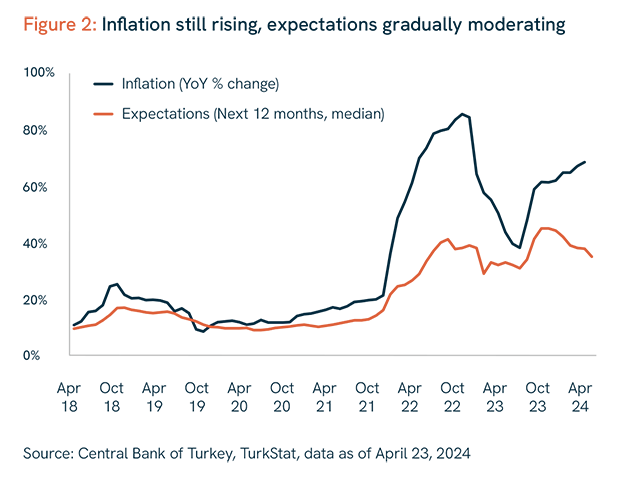

Bernard: Finance ministry officials reiterated their commitment to orthodox policies and to tackling high inflation, which also bring downside risks to growth, so the investor interest was more on the debt side (see Figure 2). Unlike Argentina, which has a midterm election in late 2025, Turkey’s next contest is four years away, providing policymakers additional runway to stay the course. This is important because Turkey’s rebalancing doesn’t need new cash, it just needs political commitment, which so far is holding. The officials stressed that disinflation would take time, which makes the lengthy electoral cycle important; they added that fiscal tightening is complementing efforts by the central bank to bring inflation lower. Relying on a stable lira as an anchor can lead to imbalances down the road, but investors seemed to think it is an acceptable risk during the early stages of the disinflation process. Generally, I sensed investors have been away from Turkey for a long time and are reassessing their exposure.

Luis: That’s a good point about fiscal and monetary policy coordination. In the U.S., the debate is about the extent to which a loose fiscal stance may be preventing inflation from easing further. That means fiscal and monetary policies are out of synch, leaving the Fed do all the heavy lifting on the disinflation front. The U.S. is running the widest fiscal deficits outside periods of war or crisis, which raises questions about sustainability and limits the degrees of freedom for when the next downturn comes.

Bernard: That’s right, with the big distinction that the dollar’s reserve currency status means the U.S. is better positioned to manage with higher for longer rates – another dimension of U.S. exceptionalism. The U.S. can muddle through, whereas the tone from EM central banks I saw in Washington had turned more cautious regarding their space to cut rates. Countries like Brazil and Mexico, who are already cutting, are signaling a shallower easing cycle, both in terms of speed and magnitude. Chile is an example of a central bank that tried to cut too aggressively, leading to a sharp devaluation in the peso, and now is also shifting its tone.

Luis: Before I let you go, how are investors thinking about geopolitical risk?

Bernard: I didn’t sense major changes regarding the active conflicts. Ukraine would get enough weapons to survive but not to win, which is more of the same. Despite direct attacks between Iran and Israel, investors’ working assumption was that Middle East tensions had peaked for the time being.

The more pressing topic was U.S.-China tensions, specifically rising concerns over China’s dumping and exporting its excess capacity in some industries like EVs. More tariffs and trade restrictions were on the way, so the question was how to position for the next protectionist wave; sanctions, however, seemed off the table for now.

Luis: Trade and financial fragmentation are secular trends we’ve been flagging for a while and they are now getting more airtime because of China’s industrial policy push focused on boosting exports of clean-tech goods, EVs, and such. As the U.S. election approaches, I expect to hear more noise about the China threat and how to deal with it. That’s a subject we can leave for another day.

Thanks for all the color, Bernard.

Bernard Steinberg

Bernard is Head of TRG’s Public Markets business and a member of the firm’s Executive Committee. He has over 30 years of experience, including 20 years of fixed income, currency, and derivative trading experience in global emerging markets. Prior to joining TRG in March 2003, Bernard was a Director in Merrill Lynch’s Emerging Markets Group and a Senior Trader with the Royal Bank of Scotland’s Emerging Markets Group. He spent seven years managing a proprietary investment portfolio for Crédit Agricole Indosuez, most recently as a Partner in the firm’s London office, where he oversaw the Local Markets Trading Group, which was responsible for a sizeable portfolio in Latin America and Eastern Europe. Bernard earned a Bachelor of Business Administration degree from Fundação Getulio Vargas Business School in São Paulo, Brazil.

Luis Arcentales

Luis has over 20 years of experience in covering global macroeconomics and markets. He is responsible for formulating market strategy at TRG. Prior to joining TRG, he had a short stint as an independent macro researcher following a nearly two-decade career at Morgan Stanley in New York. In his role as Senior Economist, his primary focus was developing the macroeconomic and political outlooks for countries in Latin America, in addition to publishing on topics ranging from the business cycle to trade dynamics for the region. Luis started his career as an equity strategist at McGlinn Capital, a value-oriented asset manager in Pennsylvania. He holds an MS in Economics and a BA in Industrial Engineering from Lehigh University; he sits on the board of Lehigh’s Martindale Center for the Study of Private Enterprise and is a CFA charter holder.

Vincent Low

Vincent has over 30 years of experience in covering global macroeconomics and markets. He is responsible for formulating investment ideas with PMs, strategists, and equity analysts and developing macro investment themes and processes for TRG’s public markets business. Prior to rejoining TRG, where he was previously CEO of its Singapore office and an Executive Committee member, Vincent held the role of Advisor to the Economics Policy Group at the Monetary Authority of Singapore. He also held roles as the Head of Currency and Fixed Income Strategy at Merrill Lynch, and Senior Economist for Southeast Asia at J.P. Morgan and Standard Chartered Bank. Vincent started his career at the Monetary Authority of Singapore in 1987 and received a Bachelor of Social Sciences in Economics from the National University of Singapore.

DISCLAIMER

The information provided herein is for educational and informational purposes only, and neither The Rohatyn Group nor any of its affiliates (together, “TRG”) is offering any product or service hereby. The information provided herein is not a recommendation, offer, or solicitation of an offer to buy or sell any security, commodity, or derivative, nor is it a recommendation to adopt any investment strategy or otherwise to be construed as investment advice. Any projections, market outlooks, investment outlooks or estimates included herein are forward-looking statements, are based upon certain assumptions, and should not be construed as an indication that certain circumstances or events will actually occur.

Other circumstances or events that were not anticipated or considered may occur and may lead to materially different outcomes. The information provided herein should not be used as the basis for making any investment decision. Unless otherwise noted, the views expressed in the content herein reflect those of the authors and participants of the conversation as of the date published and are not necessarily the views of TRG. In fact the views of TRG (and other asset managers) may diverge significantly from certain of the views expressed in the content herein. The views expressed in the content herein are subject to change without notice, and TRG disclaims any responsibility to furnish updated information in the event of any such change in views.

Certain information contained herein has been obtained from third-party sources. While TRG deems such sources to be reliable, TRG cannot and does not warrant the information to be accurate, complete or timely, and TRG disclaims any responsibility for any loss or damage arising from reliance upon such third-party information or any other content provided herein. Exposure to emerging markets generally entails greater risks and higher volatility than exposure to well-developed markets, including significant legal, economic and political risks. The prices of emerging market exchange rates, securities and other assets are often highly volatile and movements in such prices are influenced by, among other things, interest rates, changing market supply and demand, external market forces (particularly in relation to major trading partners), trade, fiscal and monetary programs, policies of governments and international political and economic events and policies. All investments entail risks, including possible loss of principal. Past performance is not necessarily indicative of future performance. The information provided herein is neither tax nor legal advice. You must consult with your own tax and legal advisors regarding your particular circumstances.