Last month brought resilience in the U.S., deflation in China, stagnation in Europe, and improved growth prospects elsewhere in emerging markets.

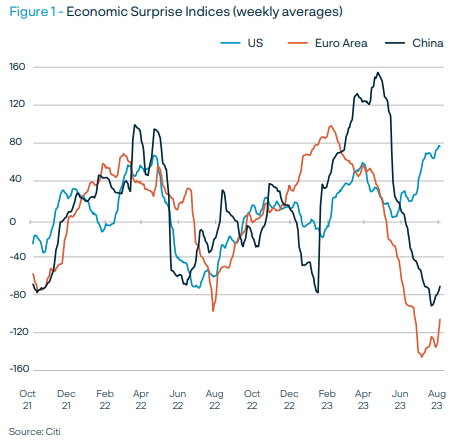

The gap between upside economic surprises in the U.S. and disappointing data from Europe is at extreme levels that have rarely been seen in the past two decades. For emerging markets (“EM”), incoming data has roughly been in line with consensus, but aggregate figures mask marked differences: news from China continues to fall short of expectations, whereas activity figures in the rest of the EM space are more upbeat. The implications for markets from diverging growth trends and asynchronous business cycles took center stage in The Rohatyn Group’s (“TRG”) August Global Strategy Meeting (“GSM”).

So far in 2023, this heterogenous growth picture has not prevented EM stocks and bonds from delivering positive returns – bonds are even outperforming stocks and government bonds. GSM participants, however, discussed that these divergent trends are likely to create a choppier investment backdrop going forward, in which selectivity remains critical. Near term, GSM contributors flagged the recent jump in U.S. long-term yields as a worrisome move that, if sustained, could become a headwind for the EM complex and risky assets.

Widening divergence

The divergence in growth performance, both within EM and between major developed market (“DM”) blocks, widened in recent months, in contrast to the more synchronized pickup seen earlier in the year. The U.S. keeps exhibiting remarkable resilience, particularly in services – even interest-rate sensitive spots like housing are inflecting higher. Conditions in Europe, meanwhile, are recessionary, and leading indicators point to sluggishness ahead. The disinflationary trend in the U.S. remains intact, whereas in Europe price pressures seem stickier. The picture in EM is similarly complex. Incoming China data is disappointing, and, based on recent market behavior, poor figures seem to raise hopes of additional stimulus. Yet so far, policy actions have been modest in scope and, TRG analysts argued, poorly structured to tackle the perceived entrenched pessimism in the private sector. Downward consensus revisions in China contrast to the slight improvement elsewhere in EM, including stronger prospects in India, Brazil, Mexico, and Indonesia. If they persist, these crosscurrents are likely to create a choppier market environment going forward, the GSM participants agreed. Another implication, some argued, is support for the dollar because the case for the euro hinges on the European Central Bank maintaining a restrictive stance – a position that looks increasingly fragile.

Growth and returns

The focus on growth trends and asynchronous cycles morphed into a discussion on their meaning for returns of various asset classes. In the U.S., still-tight labor markets and resilient activity suggest interest rates will stay higher for longer, possibly into 2024. Participants agreed that conditions for rate cuts were not present today, despite the intact disinflation trend . This implies, in turn, that the transition in the U.S. to a “reflation” regime – which favors long duration exposure as the central bank eases – is likely to take longer. Some also flagged that EM ex-China equities are outpacing China’s this year by nearly 10 percentage points, which fits with the upward GDP growth revisions in the former and downgrades in the latter. The outperformance is noteworthy because plenty of the optimism towards EM at the turn of the year depended on a strong China recovery. Some posited that China normalizing may be acting as a floor for EM growth, contrary to the uncertainty related to the lockdown policy. For Latin America at least – where bonds and stocks outperformed this year – the prices for exports (mostly commodities) remain at historically elevated levels, despite the soft patch in China.

The "issuance tantrum"

The potential fallout from the jump in U.S. Treasury yields – the 10-year benchmark approached 4.2%, nearing the October 2022 cycle high – became a hotly debated subject among GSM participants. The catalysts for the move, dubbed “issuance tantrum” by one portfolio manager, included the Bank of Japan’s new guidance and strong U.S. data. The U.S. rating downgrade and Treasury’s announcement of larger-than-anticipated auction sizes added pressure, too. While EM bond portfolio managers argued that still-high rates and central banks’ surprising larger-than-expected cuts (Chile and Brazil) meant exposure to the short end was still warranted, they also acknowledged that the narrower yield cushion between EM and DM left the asset class more vulnerable to jumps in U.S. rates. The implications for EM stocks were less straightforward since part of the U.S. bond move reflected better growth news. Until the early-August jitters, equities appeared comfortable with the prospect for elevated rates over an extended period of time (global stocks rose in tandem with nominal and real DM rates). There was at least one area of broad agreement: as much as stabilization in the U.S. long end was desirable to support market sentiment, the main risk to monitor was a shift up in short-end rates, which stayed well anchored during the recent long-bond sell-off.

Differentiation focus

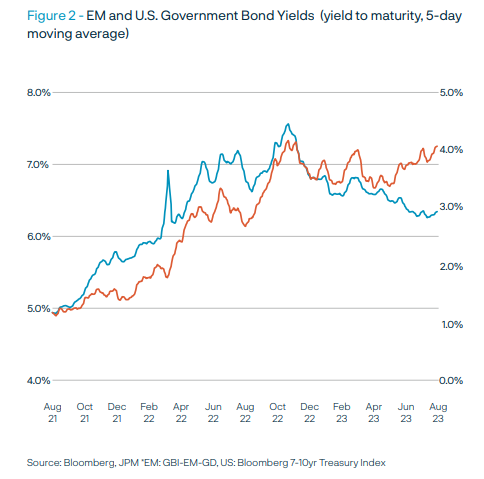

The GSM’s consensus that market conditions may become choppier reinforced the need to be selective – a recurrent theme in past discussions (see GSM July or June). There are a few reasons reinforcing the differentiation narrative, which some speakers suggested could become a more permanent feature due to the end of low rates, trade and financial fragmentation, geopolitical tensions, and higher debt burdens. First, the positive performance in EM stocks and bonds to date means valuation and yield-differential cushions are smaller, so the bar for additional gains is higher (see Figure 2). Second, EM stocks and bonds have “decoupled” from rising nominal and real yields in DM. That dynamic may change if the U.S. requires tighter financial conditions – perhaps the chief risk for markets near term – via the repricing up in terminal Federal Reserve funds. Encouragingly, that is something that has not yet happened since the move up in rates has been exclusively in longer maturities. While there is no denying the progress on the inflation front, some pointed out that recent increases in oil and grains could make the path bumpy; that is particularly the case as the Russia-Ukraine war appears to be entering a new stage as the countries target each other’s commodity-exporting infrastructure.

DISCLAIMER

The information provided herein is for educational and informational purposes only, and neither The Rohatyn Group nor any of its affiliates (together, “TRG”) is offering any product or service hereby. The information provided herein is not a recommendation, offer, or solicitation of an offer to buy or sell any security, commodity, or derivative, nor is it a recommendation to adopt any investment strategy or otherwise to be construed as investment advice. Any projections, market outlooks, investment outlooks or estimates included herein are forward-looking statements, are based upon certain assumptions, and should not be construed as an indication that certain circumstances or events will actually occur.

Other circumstances or events that were not anticipated or considered may occur and may lead to materially different outcomes. The information provided herein should not be used as the basis for making any investment decision. Unless otherwise noted, the views expressed in the content herein reflect those of the GSM participants as of the date published and are not necessarily the views of TRG. In fact the views of TRG (and other asset managers) may diverge significantly from certain of the views expressed in the content herein. The views expressed in the content herein are subject to change without notice, and TRG disclaims any responsibility to furnish updated information in the event of any such change in views.

Certain information contained herein has been obtained from third-party sources. While TRG deems such sources to be reliable, TRG cannot and does not warrant the information to be accurate, complete or timely, and TRG disclaims any responsibility for any loss or damage arising from reliance upon such third-party information or any other content provided herein. Exposure to emerging markets generally entails greater risks and higher volatility than exposure to well-developed markets, including significant legal, economic and political risks. The prices of emerging market exchange rates, securities and other assets are often highly volatile and movements in such prices are influenced by, among other things, interest rates, changing market supply and demand, external market forces (particularly in relation to major trading partners), trade, fiscal and monetary programs, policies of governments and international political and economic events and policies. All investments entail risks, including possible loss of principal. Past performance is not necessarily indicative of future performance. The information provided herein is neither tax nor legal advice. You must consult with your own tax and legal advisors regarding your particular circumstances.